New Roof Irs Depreciation

Make The Most Of Your Section 179 Tax Deduction For Orthodontic Oral Surgery Pediatric Dental Endodontic And Mo Tax Deductions Business Tax Budgeting Money

What Is The Depreciation Of The Roof On A Commercial Building

179 Tax Deduction For Commercial Roofing Projects Advanced Roofing Inc

Highland Commercial Roofing Trump Tax Code Effects On Roofing

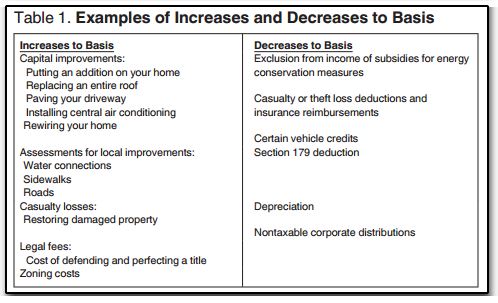

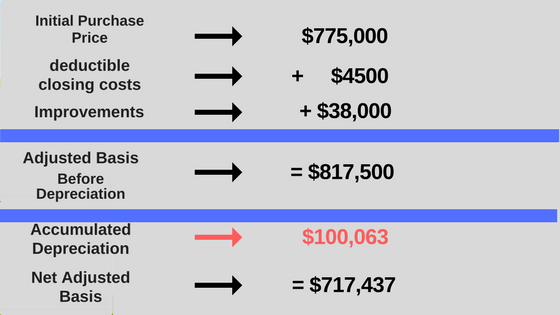

12762 Increasing Basis On An Asset Being Depreciated

Section 179d Tax Deduction For Commercial Roof Replacements

Unless an alternative depreciation method is used the cost of the new roof will be divided equally into the number of years in the recovery period and the result will be deducted as a depreciation expense each year until the roof is fully depreciated or until the property is sold or disposed of.

New roof irs depreciation.

Guide To Expensing Roofs Expense V Capitalization Section 179 D Kbkg

What You Should Know About The New Irs Depreciation Rules

Can I Deduct My New Roof On My Taxes

Tcja Expands Section 179 Expensing Strategies Csh

Depreciation Recapture What Is It And How Can I Reduce It

Pin On Home Business Essentials

Tax Advantages Of Owning Cattle Pocketsense Building A Pole Barn Old Barns Farm Life

Strawbale Cottage I Like The Idea Of A Filled Bag Built To Shape For Above Door Easier Than What We Did Cob House Plans Straw Bale House Tiny House Cabin

How The New Tax Law Affects Rental Real Estate Owners

Pin On Home Business Jobs

Home Business Ideas For Ladies 1482 20180912130128 49 Home Based Business Tax Deductions 2017 Vs 2018 Cam Interior Design Programs Interior Design Magazine

Irs Issues Guidance For Change To Real Property Depreciation Grant Thornton

Finding A Buyer To Sell Your Home Let Us Help You Find The Right Buyer To Sell Your Property At Best Possible Market Price Fo Real Estate Services Things To Sell

Congress Approves Tax Extenders For 2014 Credit Repair Improve Credit Filing Taxes

Rental Property Depreciation Rules Schedule Recapture

The 2020 Ultimate Guide To Irs Schedule E For Real Estate Investors

Pin On Home Decor

Bargins And Blessings A Combination Thrift Store And Ministry Outpost In Castroville Texas Photo By Carol M Highsmith Fe Castroville Outpost Thrifting

Tax Deductions For A Home Office Home Office Home Office Organization Office Infographic

Premier Portable Buildings Storage Parking Kenora Kijiji Portable Buildings Built In Storage Building

Building Owners Allowed To Expense New Roof In One Year

Why You Should Avoid Zillow At All Costs Huffington Post Houses In Austin Zillow Real Estate

Heatspring Magazine Finance 101 For Solar Pv Professionals

Great Pub With The Best Homemake Wine House Styles Places Around The World The Good Place

The Top 14 Rental Property Tax Deductions Investors Should Know

Wealthy Russians And South Africans Seek Portugal Golden Visa Portugal S Golden Visa Ari Scheme Launched In 2012 H Business Investment Investment Banking Visa

Http Www Saepc Org Assets Councils Southernarizona Az Library Oliverhandouts Pdf

Bonus Depreciation Kbkg

Pin On Newsrust Com World News Portal

Corn Silage Harvest 2012 Farm Pictures Farm Images Farm Life

Calculating Your Profit When Selling Your Rental Property Mortgage Blog

Section 179 Tax Deduction For Commercial Buildings Cleveland Ohio Commercial Roofing Contractor

Home Business Kuwait City 4604 20191125193313 49 Current Home Sales In My Area Wine Shop At Home Business In 2020 Story House Wine Shop At Home Best Home Business

Why Depreciation Matters For Rental Property Owners At Tax Time Stessa

What Is Rental Property Depreciation And How Does It Work

How Much Does A Mobile Home Depreciate Each Year

Small Cabins With Lofts Cabin 003sm Jpg 598 8 Kb 597 Views Cabin 017sm Jpg 406 5 Kb 529 Tiny House Inspiration Cabin Loft Shed Homes

Tax Deductible Home Improvements Granite Transformations Blog

Depreciation Strategies Under The New Tax Law What You Need To Know Counselors Of Real Estate

Turbotax Guide To Tax Deductions For Rental Property Depreciation Thestreet

Tax Implications Of Not Charging Depreciation On A Rental Property Home Guides Sf Gate

N Overview Of Tangible Property Regulations N Greatest Impacts To Your Clients N Avoid The Traps Of The Temporary Regs N Action Steps To Prepare For Ppt Download

Derksen 12x24 Lofted Small Cabin Shed Homes Diy Tiny House

Weighing Section 179 Tax Benefits Vs Bonus Depreciation Deductions For Leased Equipment Americorp Financial

Source : pinterest.com